Jayant Bhadauria, 34, head of education solutions at Adobe India, is expecting his second child this month. He has his heart set on a Shoppers' Stop pram that costs Rs 7,800. Says Bhadauria: "I liked the pram. To dish out Rs 7,800 would hurt, but since I have credit card points to redeem I don't mind the indulgence."

Credit cards don't just substitute for cash, they can also earn you reward points. "I use cards for their convenience and other benefits which I can milk," says Bhadauria. And you, too, can tap the monetary value of the points collected on your card.

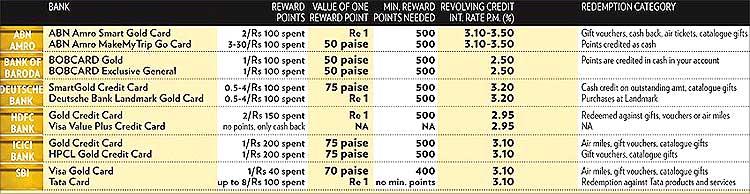

How to accumulate points?

Every time you swipe your credit card to make a purchase, you collect reward points. Typically, you get one point per Rs 100-250 spent. This, however, depends on the card and the bank. For instance, banks offer more points on co-branded cards. State Bank of India gives one point per Rs 40 spent on its Gold Card and eight points per Rs 100 on its co-branded Tata Card.

The value of each reward point also varies across credit cards and banks. Says Sachin Khandelwal, head (cards), ICICI Bank: "The value of a point can be anywhere between 30 paise to a rupee and is also a function of the merchant partner in case of co-branded cards." For example, the value of one point on the SBI Gold Card is 70 paise, while it is Re 1 on the SBI-Tata Card.

The limitation with most accelerated reward points on co-branded cards, however, is that they can be redeemed only against products and services of the partnered establishment.

One also needs to remember that points get accumulated against spends (that too, not all of them), not for cash withdrawals.

How to redeem points?

What to redeem on. Earlier, banks offered a limited catalogue of products. Plus the prices were very high and one couldn't negotiate on them. But now there is a laundry list of what you can do with the points.

For starters, there is the conventional catalogue that includes apparel, gadgets, jewellery, luggage items, and the like. You can also encash your points against gift vouchers. For instance, with HDFC Bank's Gold Card you can get gift vouchers from Domino's, Cafe Coffee Day, Pantaloons, Westside, Lee, Music World and Landmark.

Going a step further, some banks have tie-ups with certain merchants where you can redeem points instantly. You don't have to contact the bank and get vouchers; you can pay using the points.

When the card is swiped, the reward points get reflected on the machine. So, if you have accumulated points worth, say, Rs 500 and you buy goods worth Rs 1,000, the merchant will offer you the choice of using your points for payment.

Some banks now offer air tickets on reward points, a feature that was earlier limited to co-branded cards. For instance, HDFC Bank has tied up with Jet Airways, Indian and Kingfisher Airlines to allow its card users to convert their reward points into air miles. The value of one air mile is usually equal to one reward point.

"The air miles required to get complimentary tickets would depend on the airline and the travel sector," says Parag Rao, executive vice-president, head (product and portfolio management), credit cards, HDFC Bank.

Some banks, like Bank of Baroda, also let you redeem your reward points against cash. That is, cash corresponding to your reward points are credited to your account. Deutsche Bank does the same on its Gold Card, but also offers a gift catalogue.

Procedure. You can redeem your points by filling up a redemption coupon which is there on banks' website. You could also use the phone banking option. For web-enabled credit card holders redemption can happen online. The banks can take anywhere between a week to a month to redeem the points.

How to bag the best?

With so many cards, each with multiple features, how do you know which one to pick. Bhadauria wants features, flexibility and convenience from his credit cards. "Of my five cards, I use HDFC Master Titanium card the most since I can pay the bills online and it gives me higher reward points for it. The card also offers many options to redeem my points," he says.

Figure out what you want. If you are a frequent air traveler, then an airline-bank co-branded card may work for you.

Another thing to note is the value of points. Says Nirupam Sahay, chief marketing officer, SBI Cards: "Points accumulated and their value is important, in addition to the wide choice of redemption options." For example, the co-branded ABN AMRO MakeMyTrip Go Card offers three reward points per Rs 100 spent. But, on purchases made on MakeMyTrip, the points range from 10 to 30. The reward points can be redeemed as cash back into your account.

Now, more cards are offering the cash-back option on reward points. Choose the card that offers you maximum cash-back on your frequent spends and offers an array of redemption choices.

All banks display their products online and have compare tools to help you pick the best. Use these to compare the features and find the card that suits you best.

- Don't forget the expiry date. All your hard work would go waste if your points expire.

- However, most banks have started doing away with the expiry period.

- For the smart shopper, the credit card is worth more than just what it buys

© 2025

© 2025